In the third quarter of 2018, the U.S. office market again showed steady improvement, according to Transwestern’s national outlook for the sector. Absorption reached 22.7 million square feet, vacancy remained stable at 10.1%, and asking rents increased by 4.0%, annually.

Ryan Tharp, Research Director in Dallas, said the strong economy has contributed to the office market’s momentum, despite softer income growth in a very tight labor market.

“Real gross domestic product increased at an annualized 3.5%, according to first estimates, and personal consumption contributed 2.7% to that rate,” Tharp said. “Because inflation has remained in line with the Federal Reserve’s target of 2.0%, consumer and business confidence should keep the office market healthy well into 2019.”

A positive sign is that year-to-date net absorption in the office market was 17.1% higher at the end of the third quarter than it was for the same period last year. Dallas-Fort Worth, San Francisco and Denver led in absorption by a significant margin for the prior 12 months, with a combined 13.3 million square feet.

Meanwhile, demand and supply are headed for equilibrium as new construction activity peaked in early 2017. In the third quarter, only 146.3 million square feet was under construction nationally.

“It’s encouraging to see that office demand is broad-based across multiple sectors, with the technology and coworking sectors driving demand as we move later in the cycle,” said Michael Soto, Research Manager in Los Angeles. “If demand continues unabated, rental rate growth should moderate.”

Year-over-year, Minneapolis, San Antonio, and Charlotte, North Carolina, have experienced the most dramatic rent growth, all coming in at 10% or greater. The strong performance of secondary markets demonstrates that the office sector is not being propped up by a few formidable markets.

Download the national office market report at: http://twurls.com/3q18-us-

Related Stories

Market Data | Jan 6, 2022

A new survey offers a snapshot of New York’s construction market

Anchin’s poll of 20 AEC clients finds a “growing optimism,” but also multiple pressure points.

Market Data | Jan 3, 2022

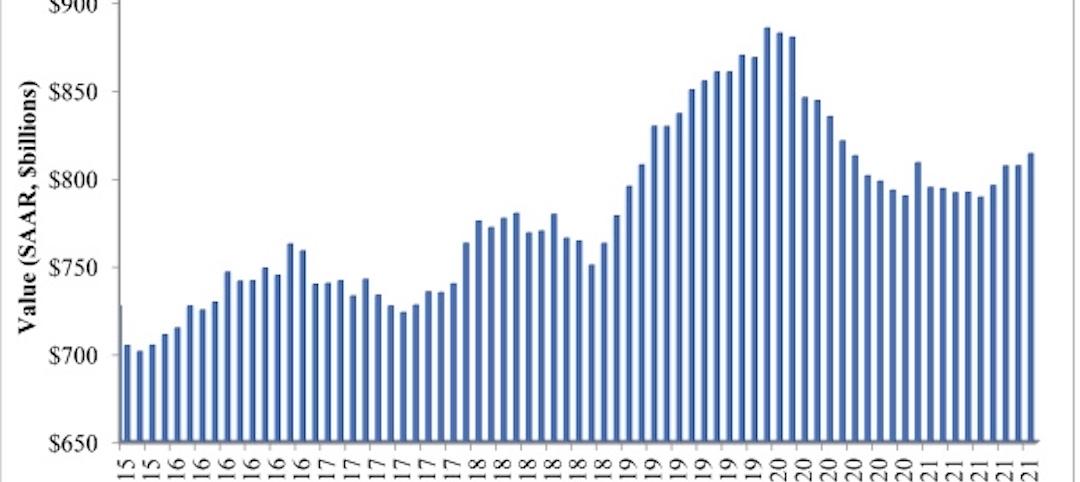

Construction spending in November increases from October and year ago

Construction spending in November totaled $1.63 trillion at a seasonally adjusted annual rate.

Market Data | Dec 22, 2021

Two out of three metro areas add construction jobs from November 2020 to November 2021

Construction employment increased in 237 or 66% of 358 metro areas over the last 12 months.

Market Data | Dec 17, 2021

Construction jobs exceed pre-pandemic level in 18 states and D.C.

Firms struggle to find qualified workers to keep up with demand.

Market Data | Dec 15, 2021

Widespread steep increases in materials costs in November outrun prices for construction projects

Construction officials say efforts to address supply chain challenges have been insufficient.

Market Data | Dec 15, 2021

Demand for design services continues to grow

Changing conditions could be on the horizon.

Market Data | Dec 5, 2021

Construction adds 31,000 jobs in November

Gains were in all segments, but the industry will need even more workers as demand accelerates.

Market Data | Dec 5, 2021

Construction spending rebounds in October

Growth in most public and private nonresidential types is offsetting the decline in residential work.

Market Data | Dec 5, 2021

Nonresidential construction spending increases nearly 1% in October

Spending was up on a monthly basis in 13 of the 16 nonresidential subcategories.

Market Data | Nov 30, 2021

Two-thirds of metro areas add construction jobs from October 2020 to October 2021

The pandemic and supply chain woes may limit gains.