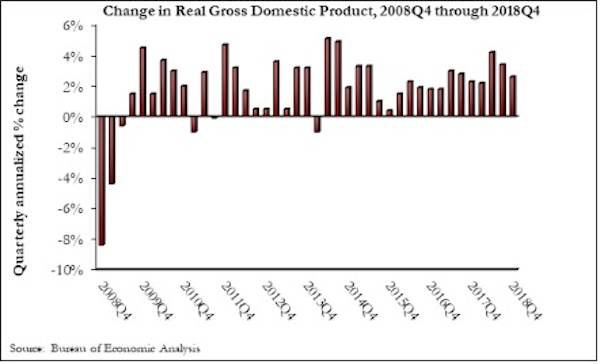

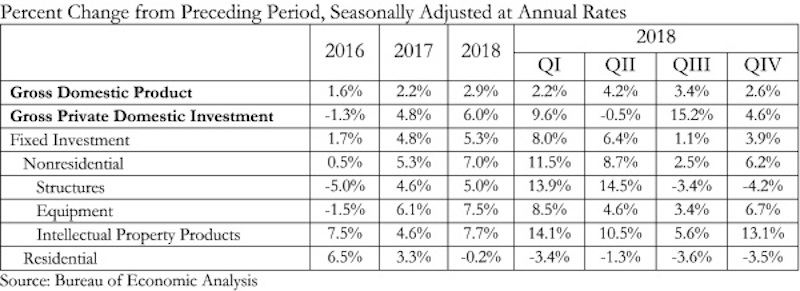

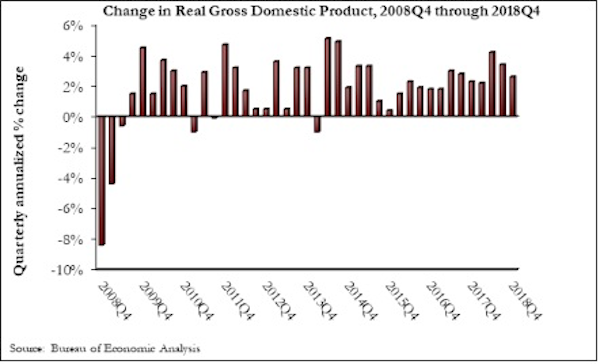

The U.S. economy grew at an annual rate of 2.6% in the fourth quarter of 2018, according to an Associated Builders and Contractors analysis of data published today by the U.S. Bureau of Economic Analysis. Year-over-year GDP growth was 3.1%, while average growth for 2018 was 2.9%.

“Today’s GDP report confirms continued strong investment in nonresidential segments in America,” said ABC Chief Economist Anirban Basu. “Separately, construction spending data show significant expenditures on the construction of data centers, hotel rooms, theme parks and fulfillment centers. These data also indicate stepped up public construction spending in categories such as transportation, education, and water systems. Despite that, today’s GDP release indicated that investment in nonresidential structures actually declined 4.2% on an annualized basis during last year’s fourth quarter. Despite that setback, this form of investment was up by 5% for the entirety of 2018.

“Undoubtedly, some attention will be given to the fact that the U.S. economy expanded by just shy of 3% in 2018,” said Basu. “Unless that figure is revised upward in subsequent releases, it will mean that America has failed to reach the 3% annual threshold since 2005. But while much attention will be given to a perceived shortfall in growth, the fourth quarter figure of 2.6% signifies that the U.S. economy entered this year with substantial momentum. Were it not for a weak residential construction sector, 3% growth would have been attained. Moreover, the data indicate strength in disposable income growth and in business investment.

“It is quite likely that the U.S. economy will expand at around 2% this year,” said Basu. “Though interest rates remain low and hiring is still brisk, a number of leading indicators suggest that the nation’s economy will soften somewhat during the quarters ahead, which can be partly attributed to a weakening global economy. This won’t unduly impact nonresidential construction activity, however, since the pace of activity in this segment tends to lag the overall economy, and strong nonresidential construction spending expected in 2019. Finally, ABC’s Construction Backlog Indicator continues to reflect strong demand for contractors, which have nearly nine months of work lined up.”

Related Stories

Market Data | Nov 22, 2021

Only 16 states and D.C. added construction jobs since the pandemic began

Texas, Wyoming have worst job losses since February 2020, while Utah, South Dakota add the most.

Market Data | Nov 10, 2021

Construction input prices see largest monthly increase since June

Construction input prices are 21.1% higher than in October 2020.

Market Data | Nov 9, 2021

Continued increases in construction materials prices starting to drive up price of construction projects

Supply chain and labor woes continue.

Market Data | Nov 5, 2021

Construction firms add 44,000 jobs in October

Gain occurs even as firms struggle with supply chain challenges.

Market Data | Nov 3, 2021

One-fifth of metro areas lost construction jobs between September 2020 and 2021

Beaumont-Port Arthur, Texas and Sacramento--Roseville--Arden-Arcade Calif. top lists of gainers.

Market Data | Nov 2, 2021

Construction spending slumps in September

A drop in residential work projects adds to ongoing downturn in private and public nonresidential.

Hotel Facilities | Oct 28, 2021

Marriott leads with the largest U.S. hotel construction pipeline at Q3 2021 close

In the third quarter alone, Marriott opened 60 new hotels/7,882 rooms accounting for 30% of all new hotel rooms that opened in the U.S.

Hotel Facilities | Oct 28, 2021

At the end of Q3 2021, Dallas tops the U.S. hotel construction pipeline

The top 25 U.S. markets account for 33% of all pipeline projects and 37% of all rooms in the U.S. hotel construction pipeline.

Market Data | Oct 27, 2021

Only 14 states and D.C. added construction jobs since the pandemic began

Supply problems, lack of infrastructure bill undermine recovery.

Market Data | Oct 26, 2021

U.S. construction pipeline experiences highs and lows in the third quarter

Renovation and conversion pipeline activity remains steady at the end of Q3 ‘21, with conversion projects hitting a cyclical peak, and ending the quarter at 752 projects/79,024 rooms.