It’s late November, which means it is market forecast season for the AEC industry. Construction outlook reports from the American Institute of Architects, Associated Builders and Contractors, ConstructConnect, Dodge Data & Analytics, and FMI are beginning to roll in. And if the early prognostications are any indication, 2018 is shaping up to be a little less rosy for the nonresidential and multifamily construction markets.

Dodge suggests the U.S. construction industry has shifted into a “mature stage of expansion.” The 11-13% annual growth in construction starts we witnessed in 2012-15 will slow to 4% in 2017 and 3% in 2018. ConstructConnect is calling for 2-3% growth in nonresidential building starts between 2018 and 2021. FMI is a bit more bullish: 5% growth in nonresidential construction spending in 2018, then 4-5% in 2019-21.

Despite the tepid outlook by construction economists—and numerous reports throughout 2017 that pointed to a looming growth slowdown for several major building sectors—optimism among AEC professionals has not waned. In fact, it has strengthened, according to a November 2017 survey of 356 architects, engineers, and contractors by Building Design+Construction.

While it has been an erratic and drama-filled first year for the Trump Administration, the vast majority of AEC professionals are not overly concerned that the Trump-led White House will negatively impact their businesses.

Six in 10 survey respondents predict that 2018 will be an “excellent” or “very good” business year for their firm. Barely half (50.3%) felt the same way this time last year, according to BD+C’s 2016 survey. Same for revenue forecasts: 62.0% predict their firm’s revenue will increase next year, and only 6.1% are calling for a drop in revenue. This is a markedly rosier outlook than last year’s, when 55.3% of respondents forecasted revenue growth and 11.5% anticipated a drop.

And while it has been an erratic and drama-filled first year for the Trump Administration—travel ban, Russian election interference probe, border wall financing fiasco, Paris Agreement withdrawal—the vast majority of AEC professionals are not overly concerned that the Trump-led White House will negatively impact their businesses. Just 16.6% of respondents cited “business impacts from the Presidential election” as a top-three concern heading into 2018. This sentiment is a somewhat dramatic turn from the post-election attitude, when nearly a third (31.7%) indicated that Trump was a major concern heading into 2017.

So, what are the top AEC business concerns for 2018? Competition from other firms (54.3%), general economic conditions (43.5%), price increases in materials and services (33.8%), and insufficient capital funding for projects (25.8%) top the list. Trump was at the bottom, along with avoiding benefit reductions, avoiding layoffs, and keeping staff motivated.

When asked about their top business development strategies for the next 12-24 months, respondents most often cited: an increase in marketing/PR efforts (47.4%), selective hires to increase competitiveness (46.3%), investment in technology (44.3%), staff training/education (43.5%), and launching a new service or business opportunity (38.0%). At the bottom: open a new office, strategic acquisition, and acquiring a new service or business opportunity.

Multifamily housing and senior living developments head the list of the hottest sectors heading into 2018, according to survey respondents. Well more than half (57.4%) indicated that the prospects for multifamily work were either “excellent” or “good” for 2018; 55.9% said the same for senior living work. Other strong building sectors: office interior/fitouts (55.2%), healthcare (50.1%), office buildings (44.5%), industrial/warehouses (44.1%), data centers (42.3%), and hotels/hospitality (41.3%). At the bottom of the list: religious/places of worship, sports/recreation, transit facilities, and cultural/performing arts buildings.

Related Stories

Industry Research | Jun 15, 2017

Commercial Construction Index indicates high revenue and employment expectations for 2017

USG Corporation (USG) and U.S. Chamber of Commerce release survey results gauging confidence among industry leaders.

Industry Research | Jun 13, 2017

Gender, racial, and ethnic diversity increases among emerging professionals

For the first time since NCARB began collecting demographics data, gender equity improved along every career stage.

Industry Research | May 25, 2017

Project labor agreement mandates inflate cost of construction 13%

Ohio schools built under government-mandated project labor agreements (PLAs) cost 13.12 percent more than schools that were bid and constructed through fair and open competition.

Market Data | May 24, 2017

Design billings increasing entering height of construction season

All regions report positive business conditions.

Market Data | May 24, 2017

The top franchise companies in the construction pipeline

3 franchise companies comprise 65% of all rooms in the Total Pipeline.

Industry Research | May 24, 2017

These buildings paid the highest property taxes in 2016

Office buildings dominate the list, but a residential community climbed as high as number two on the list.

Market Data | May 16, 2017

Construction firms add 5,000 jobs in April

Unemployment down to 4.4%; Specialty trade jobs dip slightly.

Industry Research | May 4, 2017

How your AEC firm can go from the shortlist to winning new business

Here are four key lessons to help you close more business.

Engineers | May 3, 2017

At first buoyed by Trump election, U.S. engineers now less optimistic about markets, new survey shows

The first quarter 2017 (Q1/17) of ACEC’s Engineering Business Index (EBI) dipped slightly (0.5 points) to 66.0.

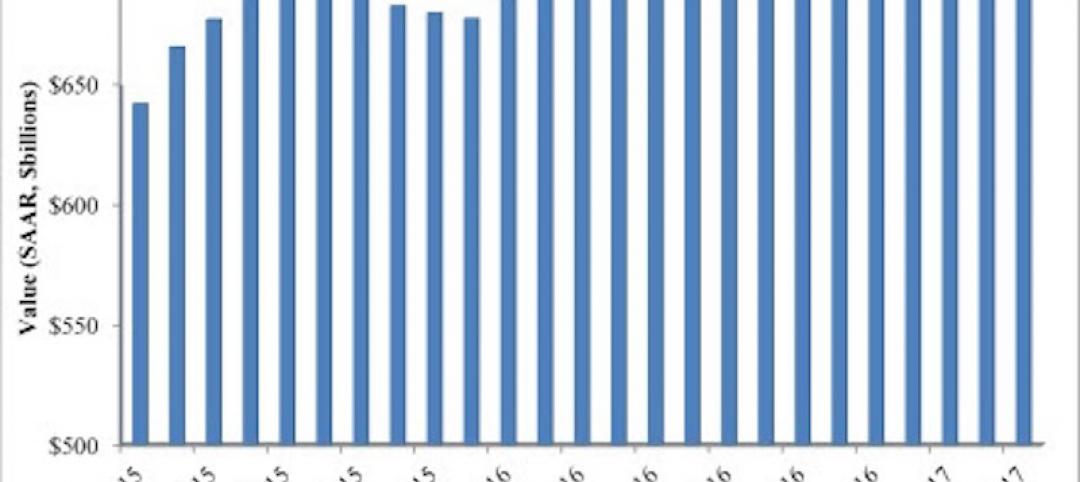

Market Data | May 2, 2017

Nonresidential Spending loses steam after strong start to year

Spending in the segment totaled $708.6 billion on a seasonally adjusted, annualized basis.