Cap rates for real estate across most asset sectors is expected to remain stable in the second half of 2015, following a first half during which the U.S. commercial real estate market continued to perform well and attract substantial investor interest.

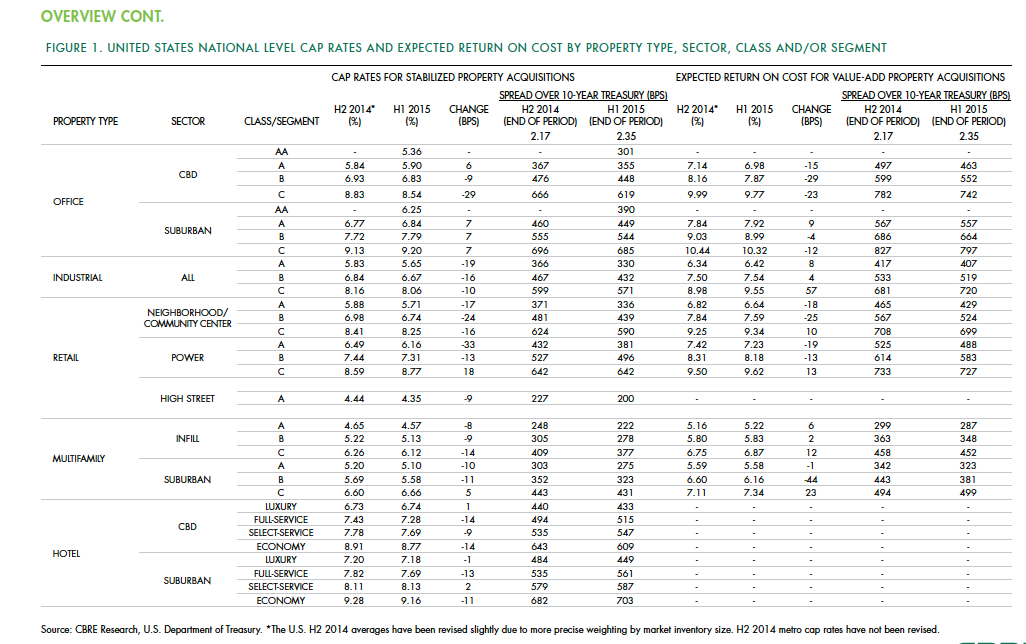

According to the CBRE North America Cap Rate Survey, which tracks activity in 46 major U.S. markets and 10 markets in Canada during the first six months of the year, national cap rates for industrial facilities in the U.S. experienced “very modest” cap-rate declines of 10 to 19 basis points. CBRE estimates that cap rates for stabilized Class A industrial assets was 5.65%.

Class A infill multifamily cap rates were 4.57% in the first half of the year, the second-lowest of all product types. The retail sector had the most significant national cap rate compression, followed by hotels. CBRE suggests that retail and hotels were the sectors that took the longest to recover from the past recession, “therefore, it is not surprising that the cap rate declines are greater in these sectors than those more mature in the real estate cycle.”

Central Business District Class B and C office cap rates were slightly off in the first half, but not Class A offices, “one example of investors moving out of on the risk curve,” CBRE notes. And despite sales volume gains, suburban office cap rates rose, on average, by 7 basis points.

Details from this report, as well as CBRE’s near-term predictions, include the following:

• Interest rates, a big demand driver in the commercial real estate space, are expected to rise modestly. The 10-year Treasury is projected to increase to 2.61% in the second half of 2015, and to 3.19% in 2016. However, “the near-term outlook of higher interest rates is not necessarily going to translate into higher cap rates if the rates come from stronger economic growth, as expected, as opposed to an unexpected shock to the economic system,” CBRE writes.

• CRBE doesn’t expect any cap rate movement in the second half of 2015 for office assets in the majority of markets, and only modest declines in those asset classes that do change. Jacksonville and Cincinnati are expected to experience the largest cap rate declines in Class A acquisitions.

• Transaction activity in the U.S. industrial sector during the first half of 2015 rose 70% to $37 billion. CBRE expects the full-year gain over 2014 to be 40% or greater. Cap rates in this sector are expected to fall modestly in more than one-third of the markets surveyed. Larger declines of 25 basis points or more are expected in Class B and C stabilized properties in Philadelphia and St. Louis. On the other hand, 58% of the market surveyed should experience no change to stabilized industrial cap rates.

• Retail investment in the first half of 2015 rose 12% to $45.6 billion. The “mall and other” category in this sector grew by 14%. CBRE expects investment to accelerate modestly through the remainder of the year. As far as cap rates are concerned, Class B experienced the largest average decline of 24 basis points. And four markets—San Jose, San Francisco, Los Angeles, and Orange County, Calif.—all had Class A caps under 5%.

• In the first six months of 2015, sales of multifamily properties jumped 38% to 63.2 billion. One-third of that capital went to mid- and high-rise projects. For Class A infill assets, San Francisco had the lowest cap rate, at 3.75%. Of the 44 markets surveyed in this sector, 33 had cap rates of 5% or less. CRBE is predicting no cap rate change for acquisitions of stabilized infill multifamily assets in the second half of the year for more than 80% of the markets surveyed. But cap compression should occur in Nashville, Washington D.C., Baltimore, Indianapolis, and Detroit.

• Investment in U.S. hotels, at $26.9 billion, was 67% higher than in the first half of 2014. The vast majority of hotel investors are domestic, especially outside of major cities. CBRE suggests, though, that hotel pricing, as measured by cap rates, has peaked for high-end products in top-tier markets. “But it’s too early to definitively make that call,” it writes. CRBE expects cap rates for acquisitions of stabilized hotel properties to remain “broadly stable” in the second half of 2015, with 62% of markets tracked experiencing no change. Any noticeable compression is likely to occur in Tier I metros like Las Vegas and Orlando, and Tier III markets such as Tampa, Jacksonville, Austin, and Pittsburgh.

Related Stories

Building Tech | Apr 13, 2016

The Hyperchair gives employees access to their own personal set of climate controls

Not only can the Hyperchair reduce heating and cooling costs and maximize employee comfort, but it can help a company become more environmentally friendly, as well.

Architects | Mar 20, 2016

Ars Gratia Artis: A North Carolina architect emphasizes the value of art in its designs

Turan Duda says clients are receptive, but the art must still be integral to the building’s overall vision.

Office Buildings | Mar 16, 2016

Google releases new plans and renderings of its Mountain View campus

The original canopy design scheme is still in place, but the plans now call for it to be opaque.

Office Buildings | Mar 10, 2016

Expedia unveils design for Seattle waterfront campus

Transparency and outdoor areas will give the complex a Pacific Northwest vibe.

Office Buildings | Mar 9, 2016

CBRE: Workplace wellness on the rise

As insurance premiums and deductibles continue to rise, both employees and employers are evaluating options to improve their wellbeing, writes CBRE Healthcare Managing Director Craig Beam.

Market Data | Mar 6, 2016

Real estate execs measure success by how well they manage ‘talent,’ costs, and growth

A new CBRE survey finds more companies leaning toward “smarter” workspaces.

Office Buildings | Mar 2, 2016

HDR redesigns Twin Cities' studio to have coffee shop vibe

With open spaces, huddle rooms, and a design lab, the firm's new digs are drastically different than the old studio, which felt like working in a law office. Design Principal Mike Rodriguez highlights HDR's renovation plan.

Office Buildings | Mar 1, 2016

SmithGroupJJR and The Christman Company create a financial headquarters without the drab

The “un-bank” design ditched the stuffy design elements typical of financial institutions and, instead, created something much more inviting.

Office Buildings | Feb 29, 2016

Mobileapolis: An open experiment in workplace mobility

Check out this fun infographic that explains Perkins+Will's ambitions, findings, and next steps for the future home of the firm's Minneapolis office.

Office Buildings | Feb 26, 2016

Benching, desking, and (mostly) paper-free: Report identifies top trends in workplace design for 2016

The report, from Ted Moudis Associates, encompasses over 2.5 million sf of workspace built over the past two years.