Though news reports and predictions painted a gloomy picture, the U.S. economy actually ended 2013 with a record setting year on Wall Street. The Dow Jones Industrial Average finished up 26.5%, its best return since 1995, and the S&P up nearly 30%, shattering previous records.

(See past articles from CBRE Healthcare)

Momentum continues to build in the housing market with positive trends in pricing, new housing starts, and inventory volume across the country. The U.S. economy added 74,000 jobs in December, as the unemployment rate fell to 6.7%, according to the Bureau of Labor Statistics.

With an improving economy and an unprecedented stimulus from the Federal Reserve continuing through 2014, the macro-economic outlook is good.

Healthcare Reform

Meanwhile, the healthcare industry has been rapidly evolving under the Affordable Care Act (ACA). Healthcare reform has compelled health systems, hospitals and physician groups to rein in sky-high costs while improving the quality of care, often coping with more regulatory requirements and less money.

Changes to reimbursement methods and reductions in healthcare provider compensation combined with an increased demand for healthcare services over the next five years, from an estimated 79 million aging baby boomers and 30 million newly insured patients, is forcing health systems to rethink their approach to balance sheet assets and liabilities, including health care real estate.

As health systems and physician groups change their delivery network, both healthcare service operators and owners of healthcare real estate are repositioning their portfolio requirements based on their growth needs. This has led to the highest medical office sales volume in the healthcare capital markets since 2007.

Healthcare reform incentives are driving consolidation of services in the industry, which has produced a robust mergers and acquisitions environment. As hospitals and healthcare organizations face mounting competitive, regulatory and financial challenges, leadership is seeking ways to capitalize on the increase of privately insured patients and Medicaid expansion while effectively serving the interests of their communities.

Healthcare operators need to diversify and expand their patient base while also becoming more efficient and leaner. This is most effectively achieved through greater economies of scale by merging with other health systems, hospitals, and physician groups, leading to a consolidation in the industry.

Consolidation is taking on two forms that are impacting real estate. First, is a unification of real estate assets as a result of health system mergers and physician employment, which has caused a consolidation of physician practices into fewer facilities that are strategically dispersed throughout the community. The other is consolidation among the hospitals and health systems seeking to concentrate operations in a single Metropolitan Statistical Area (MSA), region or state.

Off-Campus Healthcare

Healthcare investors are monitoring the consolidation trends and strategically aligning themselves through real estate transactions with market dominant hospitals and health systems, specifically those with investment grade credit ratings. Historically, investment in medical office properties revealed an institutional and REIT investor preference for core on-campus properties only.

However, over the past 12-18 months, we have witnessed little difference between core on-campus and core off-campus medical office buildings with meaningful hospital tenancy. This is a direct result of the health system shift to high quality healthcare delivered in outpatient facilities further away from traditional acute-care hospital campuses.

The care delivery network is moving from the busy, compact hospital campuses to off-campus outpatient settings with convenient access where patients live, work and shop. In response to healthcare providers commitment to off-campus destinations located near traditional retail properties and close to residential neighborhoods, investors have modified their investment criteria with a focus on off-campus properties.

The buyer pool for healthcare real estate has steadily increased over the last couple of years as investors continue to realize the inherent stability and higher returns for medical properties when compared to the more competitive multi-family, office, retail, and industrial real estate markets.

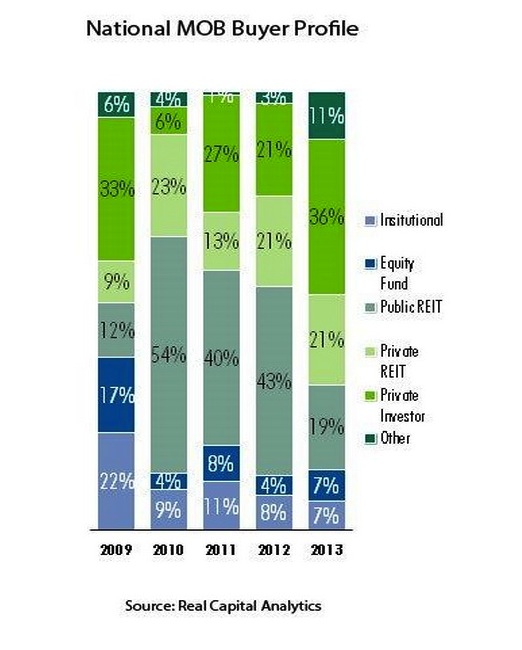

Public healthcare REITs have historically dominated the medical office investment market share, but in 2013 the private healthcare REITs and private capital investors took over the top slots. Listed and non-listed U.S. equity REITs (including both Public and Private) raised a total of $76.96 billion of equity and debt in 2013, an amount that surpassed 2012’s prior record of $73.33 billion, according to the National Association of Real Estate Investment Trusts (NAREIT). Nearly $9.3 billion, or roughly 12% was attributed to the Healthcare sector.

Conclusion

We anticipate another active year in healthcare capital markets for 2014. All investors will have stable access to capital and interest rates will likely remain at historic lows.

The favorable macro-economic outlook and consolidation among healthcare providers and continuous modification of the healthcare delivery model will continue to fuel the investment engine for what could be another record year in medical office sales.

About the authors

Lee Asher (Lee.Asher@cbre.com) and Chris Bodnar (Chris.Bodnar@cbre.com) are both Senior Vice Presidents with CBRE Healthcare Capital Markets Group. For more on CBRE Healthcare, visit www.cbre.com/healthcare.

Related Stories

K-12 Schools | Aug 29, 2024

Designing for dyslexia: How architecture can address neurodiversity in K-12 schools

Architects play a critical role in designing school environments that support students with learning differences, particularly dyslexia, by enhancing social and emotional competence and physical comfort. Effective design principles not only benefit students with dyslexia but also improve the learning experience for all students and faculty. This article explores how key design strategies at the campus, classroom, and individual levels can foster confidence, comfort, and resilience, thereby optimizing educational outcomes for students with dyslexia and other learning differences.

Museums | Aug 29, 2024

Bjarke Ingels' Suzhou Museum of Contemporary Art conceived as village of 12 pavilions

The 60,000-sm Suzhou Museum of Contemporary Art in Suzhou, Jiangsu, China recently topped out. Designed by Bjarke Ingels Group (BIG), the museum is conceived as a village of 12 pavilions, offering a modern interpretation of the elements that have defined the city’s urbanism, architecture, and landscape for centuries.

Adaptive Reuse | Aug 28, 2024

Cities in Washington State will offer tax breaks for office-to-residential conversions

A law passed earlier this year by the Washington State Legislature allows developers to defer sales and use taxes if they convert existing structures, including office buildings, into affordable housing.

Industrial Facilities | Aug 28, 2024

UK-based tire company plans to build the first carbon-neutral tire factory in the U.S.

ENSO, a U.K.-based company that makes tires for electric vehicles, has announced plans to build the first carbon-neutral tire factory in the U.S. The $500 million ENSO technology campus will be powered entirely by renewable energy. The first-of-its-kind tire factory aims to be carbon neutral without purchased offsets, using carbon-neutral raw materials and building materials.

Architects | Aug 28, 2024

KTGY acquires residential high-rise specialist GDA Architects

KTGY, an award-winning design firm focused on architecture, interior design, branded environments and urban design, announced that it has acquired GDA Architects, a Dallas-based architectural firm specializing in high rise residential, hospitality and industrial design.

K-12 Schools | Aug 26, 2024

Windows in K-12 classrooms provide opportunities, not distractions

On a knee-jerk level, a window seems like a built-in distraction, guaranteed to promote wandering minds in any classroom or workspace. Yet, a steady stream of studies has found the opposite to be true.

Building Technology | Aug 23, 2024

Top-down construction: Streamlining the building process | BD+C

Learn why top-down construction is becoming popular again for urban projects and how it can benefit your construction process in this comprehensive blog.

Airports | Aug 22, 2024

Portland opens $2 billion mass timber expansion and renovation to its international airport

This month, the Portland International Airport (PDX) main terminal expansion opened to passengers. Designed by ZGF for the Port of Portland, the 1 million-sf project doubles the capacity of PDX and enables the airport to welcome 35 million passengers per year by 2045.

Adaptive Reuse | Aug 22, 2024

6 key fire and life safety considerations for office-to-residential conversions

Office-to-residential conversions may be fraught with fire and life safety challenges, from egress requirements to fire protection system gaps. Here are six important considerations to consider.

Resiliency | Aug 22, 2024

Austin area evacuation center will double as events venue

A new 45,000 sf FEMA-operated evacuation shelter in the Greater Austin metropolitan area will begin construction this fall. The center will be available to house people in the event of a disaster such as a major hurricane and double as an events venue when not needed for emergency shelter.