Cap rates for real estate across most asset sectors is expected to remain stable in the second half of 2015, following a first half during which the U.S. commercial real estate market continued to perform well and attract substantial investor interest.

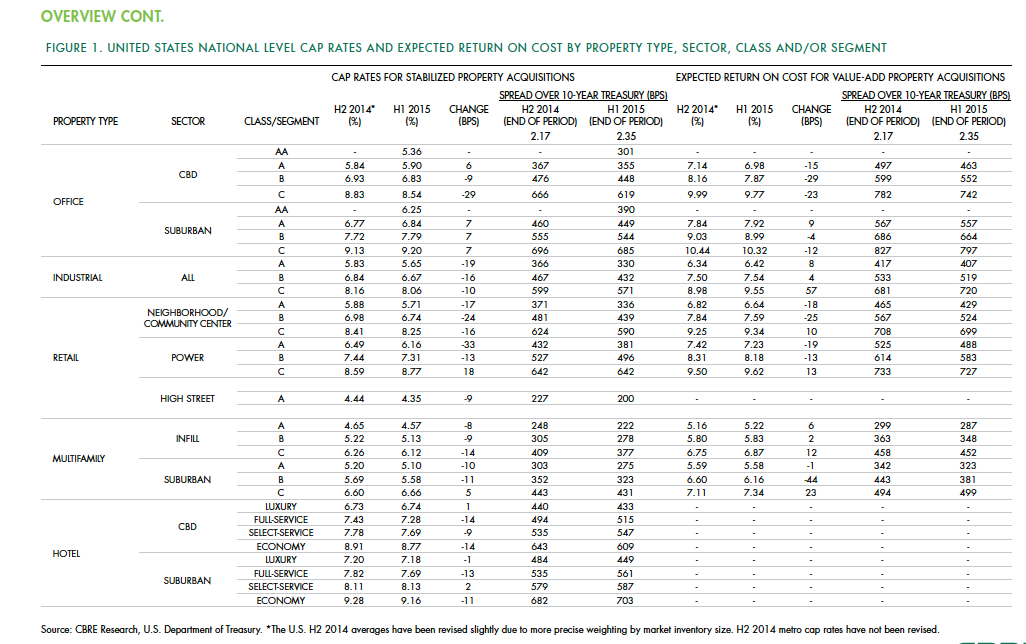

According to the CBRE North America Cap Rate Survey, which tracks activity in 46 major U.S. markets and 10 markets in Canada during the first six months of the year, national cap rates for industrial facilities in the U.S. experienced “very modest” cap-rate declines of 10 to 19 basis points. CBRE estimates that cap rates for stabilized Class A industrial assets was 5.65%.

Class A infill multifamily cap rates were 4.57% in the first half of the year, the second-lowest of all product types. The retail sector had the most significant national cap rate compression, followed by hotels. CBRE suggests that retail and hotels were the sectors that took the longest to recover from the past recession, “therefore, it is not surprising that the cap rate declines are greater in these sectors than those more mature in the real estate cycle.”

Central Business District Class B and C office cap rates were slightly off in the first half, but not Class A offices, “one example of investors moving out of on the risk curve,” CBRE notes. And despite sales volume gains, suburban office cap rates rose, on average, by 7 basis points.

Details from this report, as well as CBRE’s near-term predictions, include the following:

• Interest rates, a big demand driver in the commercial real estate space, are expected to rise modestly. The 10-year Treasury is projected to increase to 2.61% in the second half of 2015, and to 3.19% in 2016. However, “the near-term outlook of higher interest rates is not necessarily going to translate into higher cap rates if the rates come from stronger economic growth, as expected, as opposed to an unexpected shock to the economic system,” CBRE writes.

• CRBE doesn’t expect any cap rate movement in the second half of 2015 for office assets in the majority of markets, and only modest declines in those asset classes that do change. Jacksonville and Cincinnati are expected to experience the largest cap rate declines in Class A acquisitions.

• Transaction activity in the U.S. industrial sector during the first half of 2015 rose 70% to $37 billion. CBRE expects the full-year gain over 2014 to be 40% or greater. Cap rates in this sector are expected to fall modestly in more than one-third of the markets surveyed. Larger declines of 25 basis points or more are expected in Class B and C stabilized properties in Philadelphia and St. Louis. On the other hand, 58% of the market surveyed should experience no change to stabilized industrial cap rates.

• Retail investment in the first half of 2015 rose 12% to $45.6 billion. The “mall and other” category in this sector grew by 14%. CBRE expects investment to accelerate modestly through the remainder of the year. As far as cap rates are concerned, Class B experienced the largest average decline of 24 basis points. And four markets—San Jose, San Francisco, Los Angeles, and Orange County, Calif.—all had Class A caps under 5%.

• In the first six months of 2015, sales of multifamily properties jumped 38% to 63.2 billion. One-third of that capital went to mid- and high-rise projects. For Class A infill assets, San Francisco had the lowest cap rate, at 3.75%. Of the 44 markets surveyed in this sector, 33 had cap rates of 5% or less. CRBE is predicting no cap rate change for acquisitions of stabilized infill multifamily assets in the second half of the year for more than 80% of the markets surveyed. But cap compression should occur in Nashville, Washington D.C., Baltimore, Indianapolis, and Detroit.

• Investment in U.S. hotels, at $26.9 billion, was 67% higher than in the first half of 2014. The vast majority of hotel investors are domestic, especially outside of major cities. CBRE suggests, though, that hotel pricing, as measured by cap rates, has peaked for high-end products in top-tier markets. “But it’s too early to definitively make that call,” it writes. CRBE expects cap rates for acquisitions of stabilized hotel properties to remain “broadly stable” in the second half of 2015, with 62% of markets tracked experiencing no change. Any noticeable compression is likely to occur in Tier I metros like Las Vegas and Orlando, and Tier III markets such as Tampa, Jacksonville, Austin, and Pittsburgh.

Related Stories

Sponsored | | Oct 23, 2014

From slots to public safety: Abandoned Detroit casino transformed into LEED-certified public safety headquarters

First constructed as an office for the Internal Revenue Service, the city's new public safety headquarters had more recently served as a temporary home for the MGM Casino. SPONSORED CONTENT

| Oct 23, 2014

China's 'weird' buildings: President Xi Jinping wants no more of them

During a literary symposium in Beijing, Chinese President Xi Jinping urged architects, authors, actors, and other artists to produce work with "artistic and moral value."

| Oct 22, 2014

Customization is the key in tomorrow's workplace

The importance of mobility, flexibility, and sustainability in the world of corporate design are already well-established. A newer trend that’s gaining deserved attention is customizability, and how it will look in the coming years, writes GS&P's Leith Oatman.

| Oct 16, 2014

Perkins+Will white paper examines alternatives to flame retardant building materials

The white paper includes a list of 193 flame retardants, including 29 discovered in building and household products, 50 found in the indoor environment, and 33 in human blood, milk, and tissues.

| Oct 15, 2014

Harvard launches ‘design-centric’ center for green buildings and cities

The impetus behind Harvard's Center for Green Buildings and Cities is what the design school’s dean, Mohsen Mostafavi, describes as a “rapidly urbanizing global economy,” in which cities are building new structures “on a massive scale.”

| Oct 14, 2014

Proven 6-step approach to treating historic windows

This course provides step-by-step prescriptive advice to architects, engineers, and contractors on when it makes sense to repair or rehabilitate existing windows, and when they should advise their building owner clients to consider replacement.

| Oct 13, 2014

The mindful workplace: How employees can manage stress at the office

I have spent the last several months writing about healthy workplaces. My research lately has focused on stress—how we get stressed and ways to manage it through meditation and other mindful practices, writes HOK's Leigh Stringer.

Sponsored | | Oct 13, 2014

CLT, glulam deliver strength, low profile, and aesthetics for B.C. office building

When he set out to design his company’s new headquarters building on Lakeshore Road in scenic Kelowna, B.C., Tim McLennan of Faction Projects knew quickly that cross-laminated timber was an ideal material.

| Oct 12, 2014

AIA 2030 commitment: Five years on, are we any closer to net-zero?

This year marks the fifth anniversary of the American Institute of Architects’ effort to have architecture firms voluntarily pledge net-zero energy design for all their buildings by 2030.

| Oct 9, 2014

Regulations, demand will accelerate revenue from zero energy buildings, according to study

A new study by Navigant Research projects that public- and private-sector efforts to lower the carbon footprint of new and renovated commercial and residential structures will boost the annual revenue generated by commercial and residential zero energy buildings over the next 20 years by 122.5%, to $1.4 trillion.